Can a Torn or Damaged Will Still Be Valid?

A last will and testament is designed to ensure your wishes are carried out after your death, but what happens if the document becomes torn, stained, water-damaged, or otherwise compromised? Many people worry that physical damage automatically makes a will invalid. In reality, the answer depends on the extent of the damage, the condition of the document, and the laws that apply where the will is being probated.

If a will is damaged, it does not necessarily mean your estate plan is no longer enforceable. However, significant damage can create legal questions that may require additional review by the probate court.

Minor Damage Usually Doesn't Invalidate a Will

Everyday wear and tear is common, especially if a will has been stored for many years. A small tear, faded ink, water spots, or a wrinkled appearance generally does not affect the document's validity, provided the important information remains readable.

As long as the signatures, witness information, and the contents of the wi...

What Happens If You Lose a Last Will and Testament?

A last will and testament is one of the most important legal documents you can create. It outlines how you want your assets distributed, names an executor to manage your estate, and may include guardianship preferences for minor children. But what happens if the original will cannot be found after your death? While losing a will does not automatically mean your wishes are ignored, it can make the probate process more complicated.

Understanding the potential consequences can help you take steps to protect your estate plan and avoid unnecessary delays for your loved ones.

Why the Original Will Matters

In many jurisdictions, the original signed will is the document that a probate court expects to see. The original helps confirm that the will was properly executed and has not been altered. If only a copy is available, the court may require additional evidence before accepting it.

Depending on local laws, the court may presume that a missing original was intentionally destroyed by the p...

How Buying Property Affects Your Estate Plan

Purchasing real estate is a significant financial milestone, whether it's your first home, a vacation property, or an investment property. While buyers often focus on mortgages, inspections, and closing costs, it's equally important to consider how a new property fits into your estate plan. Updating your estate planning documents after acquiring real estate can help ensure your assets are managed and distributed according to your wishes.

Here are some key ways buying property can affect your estate plan.

Ownership Matters

The way you hold title to a property plays a major role in what happens to it after your death. Depending on the ownership structure, the property may pass directly to a surviving co-owner or become part of your estate. Common forms of ownership include sole ownership, joint ownership, and ownership through a trust or business entity.

Because each option has different legal and financial implications, it's important to understand how your choice aligns with your o...

What Makes a Will Legally Valid in California?

Creating a will is one of the most important steps in an estate plan. It allows you to specify how you want your property distributed after your death, name a guardian for minor children, and appoint someone to carry out your wishes. However, a will must meet California's legal requirements to be considered valid. Understanding these rules can help you create a document that accurately reflects your intentions and reduces the likelihood of disputes during the probate process.

You Must Have the Legal Capacity to Make a Will

In California, the person creating a will, known as the testator, must generally be at least 18 years old. They must also have the mental capacity to understand that they are making a will, recognize the nature and extent of their property, and identify the people or organizations who may inherit from their estate.

Mental capacity is assessed at the time the will is signed. Even if a person has experienced periods of illness or memory loss, they may still be able ...

What Estate Planning Attorneys Want Blended Families to Know

Blended families often bring together spouses, children, stepchildren, and shared financial responsibilities, creating a unique family dynamic. While these relationships can be rewarding, they can also make estate planning more complex. What works for a traditional estate plan may not fully address the needs of a blended family. Estate planning attorneys frequently emphasize that careful planning is essential to protect loved ones, minimize confusion, and ensure assets are distributed according to a family's wishes.

Every Family Situation Is Unique

One of the most important things estate planning attorneys want blended families to understand is that there is no one-size-fits-all solution. Each family has different relationships, financial circumstances, and goals.

Some parents want to ensure that their current spouse is financially secure while also preserving assets for children from a previous relationship. Others may wish to provide equally for all children, including stepchildre...

Why a Will Alone May Not Be Enough for Blended Families

Blended families are becoming increasingly common, bringing together spouses, children, and extended family members from different backgrounds and relationships. While these families often create strong and supportive bonds, they can also face unique estate planning challenges. Many people assume that having a will is enough to ensure their wishes are carried out after they pass away. However, for blended families, a will alone may not provide the level of protection and clarity needed to address complex family dynamics and financial goals.

The Unique Challenges of Blended Families

Estate planning for blended families often involves balancing the needs of a current spouse with the desire to provide for children from previous relationships. Without careful planning, assets may not be distributed as intended.

For example, a parent may want to leave financial support for a surviving spouse while also ensuring that children from a prior marriage eventually receive a portion of the estat...

Why Conversations About End-of-Life Wishes Matter

Talking about end-of-life wishes is one of the most difficult conversations many families avoid. The topic can feel emotional, uncomfortable, or even frightening. Yet these discussions are incredibly important. Having open and honest conversations about medical care, financial decisions, funeral preferences, and personal values can provide clarity and peace of mind for everyone involved.

End-of-life planning is not only about preparing for death. It is about protecting dignity, reducing confusion, and helping loved ones make informed decisions during emotionally stressful times. When people clearly communicate their wishes in advance, families are less likely to experience conflict, uncertainty, or guilt later on.

Reducing Stress During Difficult Times

When a medical emergency or serious illness occurs, family members are often forced to make major decisions quickly. Without prior conversations, they may struggle to guess what their loved one would have wanted. This uncertainty can ...

The Role of Coordination in a Complete Estate Plan

Estate planning is often associated with writing a will or deciding who inherits property after death. While those are important pieces, a truly complete estate plan goes far beyond a single document. One of the most overlooked yet essential aspects of estate planning is coordination. Without proper coordination between legal documents, financial accounts, insurance policies, and family intentions, even the most carefully prepared plan can create confusion or conflict later on.

Coordination in estate planning means making sure every part of the plan works together smoothly. It involves aligning beneficiary designations, trusts, wills, healthcare directives, tax strategies, and financial goals into one organized structure. When all the moving parts are connected properly, families are more likely to avoid delays, legal disputes, and unintended consequences.

Why Coordination Matters

Many people assume that once they create a will, their estate plan is complete. However, assets such as...

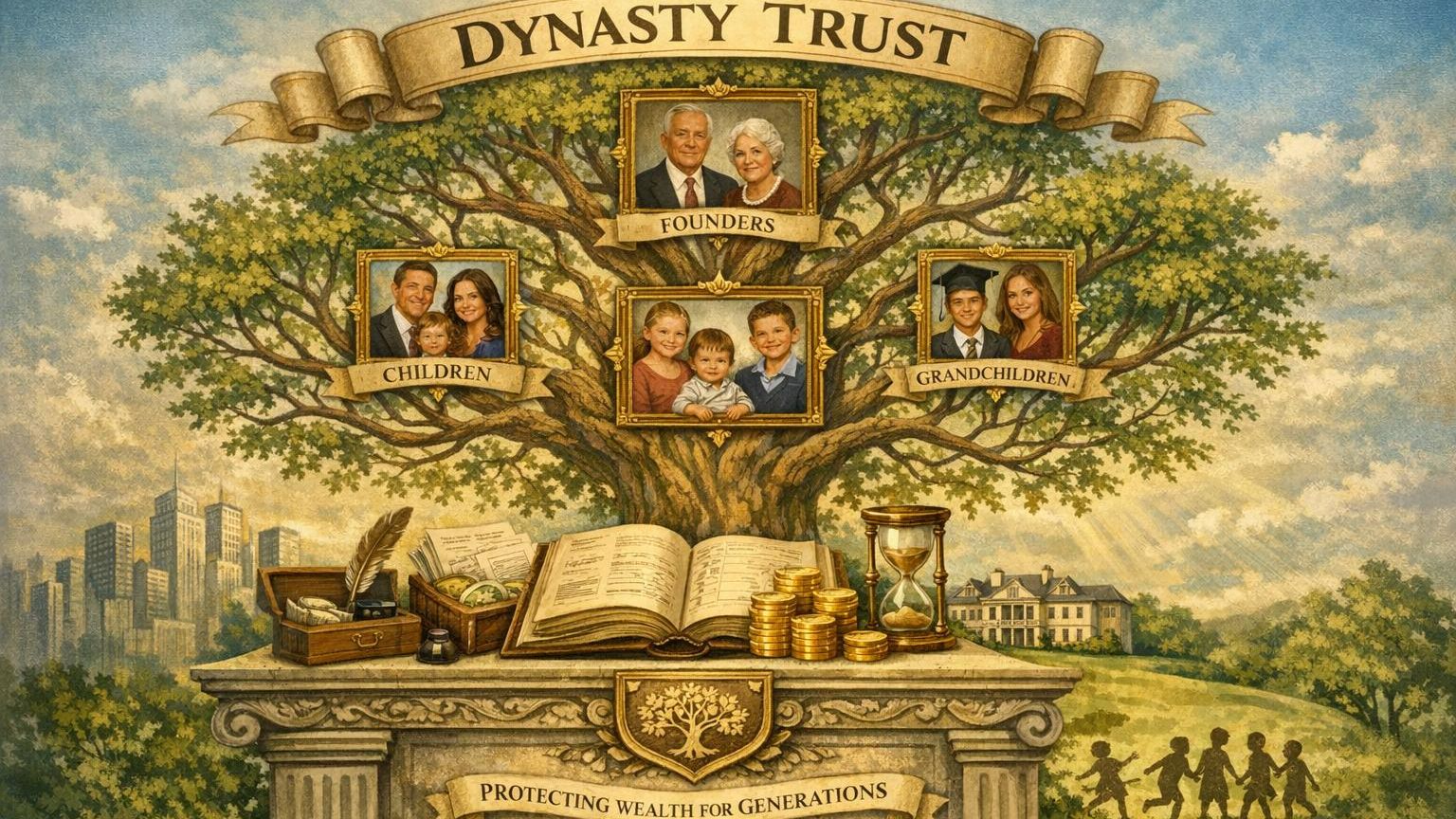

How Dynasty Trusts Preserve Wealth Across Generations

A dynasty trust is a long-term estate planning tool designed to hold and manage wealth for multiple generations of a family. Unlike a traditional trust that may end after a set period or when a beneficiary reaches a certain age, a dynasty trust can continue for decades or even indefinitely, depending on local laws. Its purpose is simple: keep assets protected, growing, and within the family line for as long as possible.

Why Families Use Dynasty Trusts

At its core, a dynasty trust is about control and continuity. Instead of passing wealth outright to heirs, which can lead to quick spending or mismanagement, assets remain inside the trust. This structure ensures that each generation benefits from the wealth without having unrestricted access to it. It’s especially appealing for families who want to build a lasting financial legacy rather than a one-time inheritance.

Another key advantage is protection. Assets held in a properly structured dynasty trust are generally shielded from cred...

Leaving Assets to Minor Children: Smart Legal Strategies

Planning how to leave assets to minor children isn’t as simple as naming them in a will. Children under 18 typically can’t legally manage significant assets, which means without proper planning, a court may step in to decide how those assets are handled. That process can be slow, expensive, and not always aligned with your intentions. A thoughtful strategy helps protect both the money and the child’s future.

Why Direct Inheritance Can Be Problematic

If you leave assets directly to a minor, the law usually requires a guardian or conservator to manage those funds until the child reaches adulthood. While that might sound reasonable, it comes with drawbacks. Court supervision can limit flexibility, add administrative costs, and create delays in accessing funds for important needs like education or healthcare.

There’s also the issue of maturity. Turning 18 doesn’t automatically mean a young adult is ready to manage a large inheritance. Without safeguards, funds could be spent quickly or ...